By: Evan Lustig

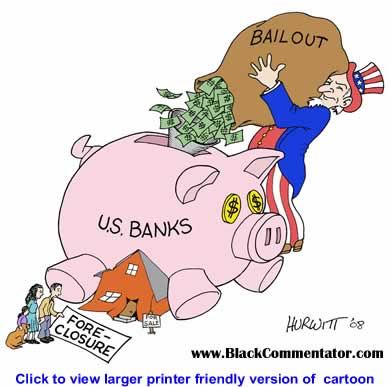

ZERO ACCOUNTABILITY! This is a charge that many of the bankers who work in finance have become comfortable with. 2008 is a year that will be remembered for the financial crisis that sparked what could possibly be the largest recession since the great depression. These bankers have watched while their clients have lost the majority of their portfolios. While their clients have been dealing with the repercussions of losing this money these bankers are still raking in the big bucks. Bankers and financial institutions are still taking bonuses and spending money to advance the institution. “79% of Wall Street workers who responded to a poll by eFinancialCareers.com said they received a bonus for 2008, despite the carnage.” One question that I’ve been pondering is, how can these bankers afford to take bonuses when all their clients are being hit by record losses? How can Citigroup afford a new plane when they are laying-off thousands of workers? The answer to this question is zero accountability. These bankers don’t care about their clients and the consumers because they will still get theirs at the end of the day. The success and money these bankers earn should directly correlate to money they make their clients. In order to fix the problem you must make it that these bankers depend on their clients and companies success to put food on the dinner table. This will help the economy cause instead of seeing each client as just another number they will see each client as a way to send their kid to college. If changes don’t occur to directly connect the bankers success to their clients the consumers will eventually lose faith in the financial industry and be unwilling to invest making it even harder for our economy to rebound from this recession.

{kind=link}